.png)

Digital onboarding has evolved from manual, branch-based customer verification processes into a technology-driven approach that improves speed, security, and compliance. Advances in digital KYC, AI, automation, and identity verification technologies are reshaping how financial institutions onboard customers and manage regulatory requirements.

The financial services industry has seen some major changes over the last few decades, with digital onboarding playing a central role in this transformation. In the past, onboarding new customers in banking was a slow, manual process involving in-person identity verification and the handling of sensitive documents. The introduction of digital onboarding has enabled financial institutions to automate many onboarding tasks, improving speed, operational efficiency, and security.

This article looks at how digital onboarding has evolved in financial services, tracing its roots from manual KYC (Know Your Customer) procedures to the advanced solutions we have today, which incorporate AI, blockchain, and biometric authentication.

Key Takeaways

- Digital onboarding has evolved from manual, branch-based processes to technology-driven experiences that improve speed, accessibility, and operational efficiency for financial institutions and customers.

- Digital KYC has transformed identity verification by automating customer checks, reducing manual effort, and helping organizations meet regulatory requirements more efficiently.

- Advances in AI, machine learning, and automation have strengthened fraud detection, risk assessment, and compliance monitoring throughout the onboarding journey.

- Financial institutions continue to face challenges related to data privacy, cross-border compliance, and cybersecurity as digital onboarding becomes more widespread.

- Emerging technologies such as AI, RegTech, blockchain, and biometric verification are shaping the future of digital onboarding and redefining how organizations verify and onboard customers.

How has digital onboarding transformed the banking sector?

The digital transformation of the banking sector is largely shaped by advancements in technology, especially in how customers are onboarded. In the past, this process required customers to visit a bank branch, fill out forms, submit identification documents, and wait for verification. It was time-consuming, inconvenient, and often prone to human error.

With the move to digital onboarding, banks and financial institutions can now offer a seamless online experience. This shift has fundamentally changed how financial institutions acquire and onboard customers. No longer do customers need to take time off work or travel to a branch to open an account or apply for financial products. Instead, they can complete the entire process from their smartphones or computers, whenever and wherever it suits them.

How has digital onboarding improved customer experiences and streamlined operations?

Digital onboarding has transformed the customer experience by removing the need for physical visits and the long waits that often accompany them. Now, customers can interact with their bank or financial institution at a time that suits them, using simple, intuitive online platforms. For financial institutions, this shift brings a host of operational advantages:

- Efficiency: Automation of identity verification and document handling speeds up the onboarding process.

- Cost reduction: Digital systems reduce the need for in-person interactions and paperwork, leading to cost savings.

- Accessibility: Digital onboarding platforms are available around the clock, giving customers the flexibility to complete the process at their own pace.

For customers, digital onboarding provides a faster, more convenient way to access financial products and services. For banks and financial institutions, it means greater operational efficiency, quicker service, and ultimately, happier customers.

How has digital onboarding impacted regulatory compliance and security?

While digital onboarding improves efficiency and accessibility, it also introduces new compliance, privacy, and security considerations for financial institutions. Financial institutions must align processes with key regulations, balancing compliance and security to protect both business and customers. As cyber threats evolve, staying vigilant and proactive is essential.

What regulatory challenges do digital KYC solutions face today?

Digital KYC solutions are built to streamline identity verification, ensuring financial institutions meet regulatory requirements with ease. However, there are a few key challenges to consider:

- Data privacy concerns: Protecting customers’ personal information is paramount, especially when complying with privacy regulations such as GDPR.

- Cross-border compliance: With regulations differing across borders, it can be tricky for banks operating internationally to establish a uniform process.

- Data accuracy: Maintaining accurate, complete, and verifiable customer information remains essential for both regulatory compliance and effective risk management.

In overcoming these challenges, it’s crucial for businesses to stay ahead, ensuring they meet both compliance and customer expectations.

.webp)

What security concerns arise as digital onboarding becomes more mainstream?

As digital onboarding becomes increasingly common, financial institutions are confronted with a range of security risks that can’t be ignored:

- Identity theft: Fraudsters can use stolen or synthetic identities to open fraudulent accounts, putting customers at risk.

- Data breaches: Cybercriminals may target banks to steal sensitive customer data, causing significant damage to both reputation and trust.

- Social engineering attacks: Attackers can manipulate employees or customers into revealing sensitive information, often exploiting human error.

- Mobile device security: With more people accessing banking services through their smartphones, securing mobile devices has become a major concern.

Addressing these risks is essential for protecting customer data, maintaining trust, and supporting regulatory compliance.

How has digital onboarding redefined KYC processes?

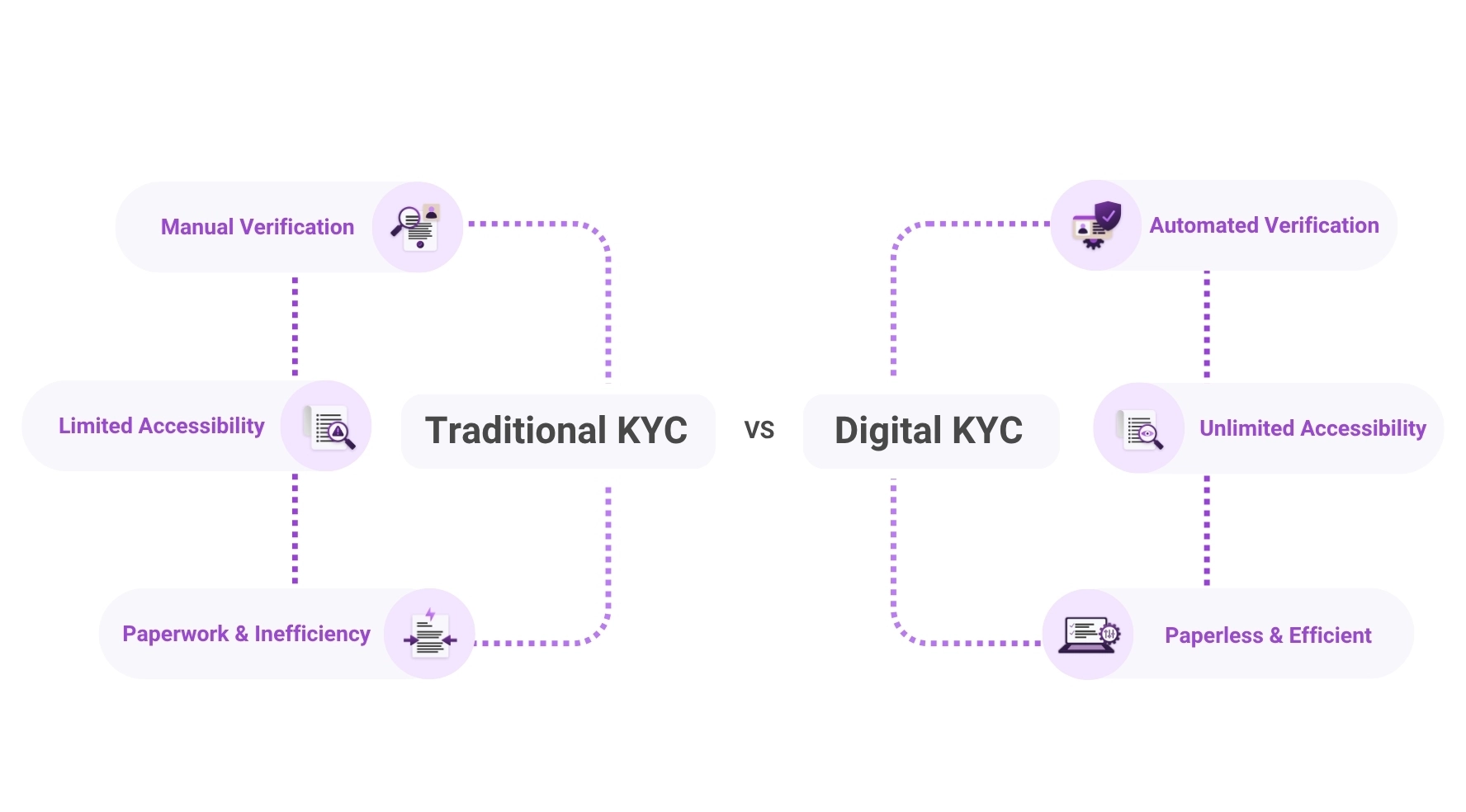

Traditional KYC processes were labor-intensive and relied heavily on paper-based documentation, leading to delays, errors, and inefficiencies. Customers were often required to visit a branch in person to provide physical identification, while banks took on the cumbersome task of manually verifying each piece of information.

The shift to digital KYC has tackled many of these issues. By automating identity verification, digital KYC has made the process faster, more accurate, and more convenient for both banks and customers alike.

Here’s a breakdown of some of the key problems with traditional KYC and how digital solutions have addressed them:

- Manual verification: In traditional KYC, human error and slow processing were common. Digital KYC uses automated tools to verify documents and cross-check customer data in real time, reducing the likelihood of mistakes.

- Limited accessibility: Customers once had to visit branches to complete KYC checks. Digital KYC allows them to complete the process from anywhere, at any time, via secure digital platforms.

- Paperwork and inefficiency: Traditional KYC was weighed down by physical paperwork, resulting in slow processing. Digital KYC eliminates paper-based processes by digitizing documents and storing them securely in the cloud, speeding up verification and improving efficiency.

Digital KYC has significantly boosted the speed, accuracy, and convenience of identity verification, streamlining the entire customer onboarding process.

How has digital KYC enhanced efficiency and compliance?

Digital KYC has transformed how financial institutions manage regulatory requirements, making it simpler to stay compliant while maintaining efficiency. By automating processes, it reduces the need for manual intervention, speeds up verification times, and minimizes errors. This ensures that institutions can meet KYC, AML, and CDD standards with ease.

Here’s how digital KYC drives both efficiency and compliance:

- Real-time identity verification: Automated verification processes enable financial institutions to swiftly and accurately validate customer identities, ensuring they meet regulatory requirements.

- Fraud detection: By leveraging AI, digital KYC can detect potential fraudulent activity during the onboarding process, enhancing security.

- Compliance management: Digital KYC platforms continuously monitor customer data, ensuring ongoing compliance with relevant laws and regulations.

Automated KYC processes help financial institutions improve operational efficiency while supporting compliance with evolving regulatory requirements.

How have KYC, AML, and CDD evolved to fight fraud in digital onboarding?

KYC, AML (Anti-Money Laundering), and CDD (Customer Due Diligence) processes have come a long way in the fight against fraud, especially in digital onboarding. Thanks to innovative tools and technologies, financial institutions are now able to spot fraudulent activity much earlier in the customer journey. Here’s how these processes have evolved:

- AI-driven fraud detection: AI systems analyze vast amounts of data to identify suspicious patterns and behaviors. By flagging unusual transactions or discrepancies, AI helps prevent fraud before it happens.

- Advanced document verification: Using optical character recognition (OCR) and machine learning, financial institutions can verify the authenticity of documents like IDs, utility bills, and bank statements in real-time.

- Real-time screening for AML: Automated systems monitor customers against global watchlists and databases for potential money laundering activity, enhancing AML compliance.

- Behavioral analytics: By tracking customer behavior during the onboarding process (e.g., typing speed, navigation patterns), institutions can detect anomalies that could signal fraudulent intent.

- Multi-layered verification: Implementing multiple methods of verification (e.g. SMS verification, document scans) helps build a stronger defense against fraud.

These advances have made KYC, AML, and CDD much more efficient, enabling financial institutions to tackle fraud without compromising the customer experience.

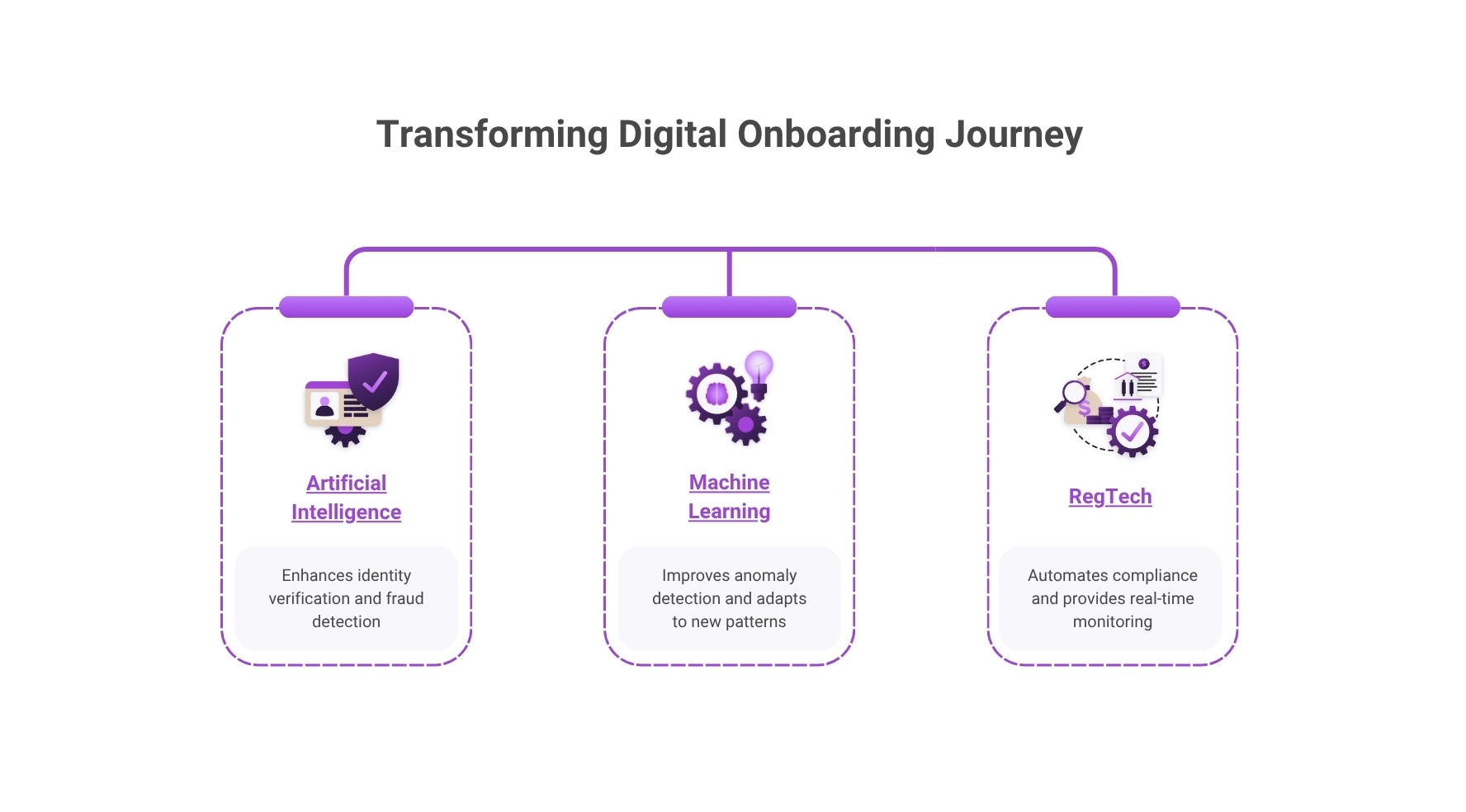

What new innovations are reshaping the digital onboarding journey?

AI, machine learning, and RegTech are reshaping how digital onboarding works, streamlining key steps, boosting fraud detection, and ensuring compliance with the latest regulations. These technologies work hand in hand to deliver a smoother, more secure, and customer-friendly onboarding experience.

Artificial Intelligence (AI):

- Identity verification: AI can swiftly scan documents and confirm identities in real-time, cutting down on errors and delays.

- Fraud detection: AI models are capable of spotting suspicious patterns and flagging potential fraud before it occurs.

- Risk assessment: By analyzing large amounts of data, AI helps banks evaluate the risk profile of each customer, enabling more informed decisions during onboarding.

Machine Learning:

- Anomaly detection: Machine learning picks up on unusual customer behavior, helping detect potential fraudulent activity.

- Continuous improvement: As it processes more data, machine learning improves over time, getting better at identifying fraud and adapting to new patterns.

RegTech:

- Regulatory compliance automation: RegTech ensures banks stay up-to-date with changing regulations, automating compliance tasks and minimizing human error.

- Monitoring and reporting: These platforms provide real-time monitoring of transactions and customer activity, offering an ongoing audit trail to ensure compliance.

Together, these technologies are helping financial institutions deliver more efficient onboarding experiences while strengthening compliance and fraud prevention capabilities.

What role does blockchain play in the future of KYC and digital onboarding?

Blockchain is becoming essential for the future of KYC and digital onboarding. Its decentralized and tamper-proof structure ensures that identity data stays secure and unchangeable. With blockchain, financial institutions can make the identity verification process quicker and safer, cutting down on fraud risks.

Here’s how blockchain can improve KYC and onboarding:

- Immutable records: Once a customer’s identity is verified on the blockchain, it can’t be changed, guaranteeing data integrity.

- Faster verification: Blockchain allows for instant identity checks, thanks to a decentralized, universally accessible network of verified identities.

- Cross-border compliance: Blockchain makes verifying identities across borders easy, simplifying compliance for multinational institutions.

- Fraud prevention: The transparency and security of blockchain make it far harder for fraudsters to manipulate documents or identities.

As adoption increases, blockchain has the potential to strengthen identity verification, improve data integrity, and support more efficient compliance processes across financial services.

Conclusion

The evolution of digital onboarding has transformed how financial institutions verify identities, meet regulatory requirements, and deliver customer experiences. What began as a manual, paper-based process has evolved into a technology-driven approach that improves efficiency, strengthens security, and supports compliance across the customer lifecycle.

As digital onboarding continues to evolve, financial institutions need solutions that can balance customer experience, compliance, security, and operational efficiency. The ability to automate identity verification, support regulatory requirements, and reduce onboarding friction is becoming increasingly important as customer expectations and compliance obligations continue to grow.

OnBoard by MVSI is an end-to-end merchant onboarding and compliance platform for regulated payments, fintech, and financial services, combining digital onboarding, KYB, AML screening, underwriting, and ongoing due diligence (OCDD) in one system.

By centralizing onboarding, identity verification, compliance screening, and risk management workflows, organizations can create more efficient onboarding experiences while maintaining strong compliance and security controls.

Disclaimer: This article is provided for informational purposes only and does not constitute legal, regulatory, compliance, or risk management advice. Regulatory requirements relating to customer onboarding, identity verification, KYC, AML, and data privacy vary across jurisdictions. Organizations should consult qualified legal, compliance, and risk professionals when implementing or updating digital onboarding processes.

Frequently Asked Questions

How does digital KYC support regulatory compliance?

Digital KYC automates identity verification, customer screening, and compliance checks, helping financial institutions meet KYC, AML, and Customer Due Diligence (CDD) requirements more efficiently. Automated processes can also reduce manual errors and improve compliance consistency.