.png)

Merchant onboarding and underwriting are crucial steps for payment providers and financial institutions. In the past, these processes were heavily reliant on paperwork, manual decision-making, and lengthy verification steps. While this method worked to an extent, it often led to inefficiencies, human error, and delays—issues that become more pronounced as businesses grow. With the rise of digital solutions, the traditional merchant underwriting process is being replaced by automated, AI-powered systems that simplify and accelerate the process.

Key Takeaways

- Traditional merchant underwriting relies on paperwork and manual reviews, often leading to inefficiency, human error, and slow approvals.

- Manual processes create costly delays and inconsistent decisions, making it harder to spot fraud and raising compliance risks.

- Technology-driven underwriting uses AI and automation to analyse merchant documents, generate accurate risk scores, and detect fraud in real time.

- Digital onboarding streamlines data collection, reduces paperwork, and speeds up merchant application approvals, improving efficiency and scalability.

- Security improves with biometric verification and continuous monitoring, ensuring fraud prevention and stronger compliance outcomes.

What is Merchant Underwriting?

The merchant underwriting process is a vital procedure for risk and compliance teams at payment providers and financial institutions. For compliance teams, it is the line of defense that prevents risky or unstable merchants from slipping through. Without it, the risks of fraud, chargebacks, financial instability, and regulatory breaches grow. These issues threaten trust and expose institutions to damaging consequences.

The process typically includes:

- Financial Evaluation: A thorough look into the merchant’s financial health, creditworthiness, and overall stability.

- Risk Profiling: Identifying potential risks, such as high chargeback rates, involvement in high-risk sectors (like gambling or adult entertainment), or any other issues that might pose a threat to financial or operational stability.

- Compliance Verification: Ensuring the merchant meets industry regulations such as Know Your Customer (KYC) and Anti-Money Laundering (AML) laws.

- Operational Review: A close inspection of the merchant's business model, products, services, and practices to gauge their impact on platform stability and reputation.

Merchant underwriting is foundational for safeguarding the integrity of payment systems and ensuring operational stability. Effective merchant underwriting is not just about compliance—it's about risk management, protecting reputation, and maintaining the financial and operational health of the entire payment ecosystem.

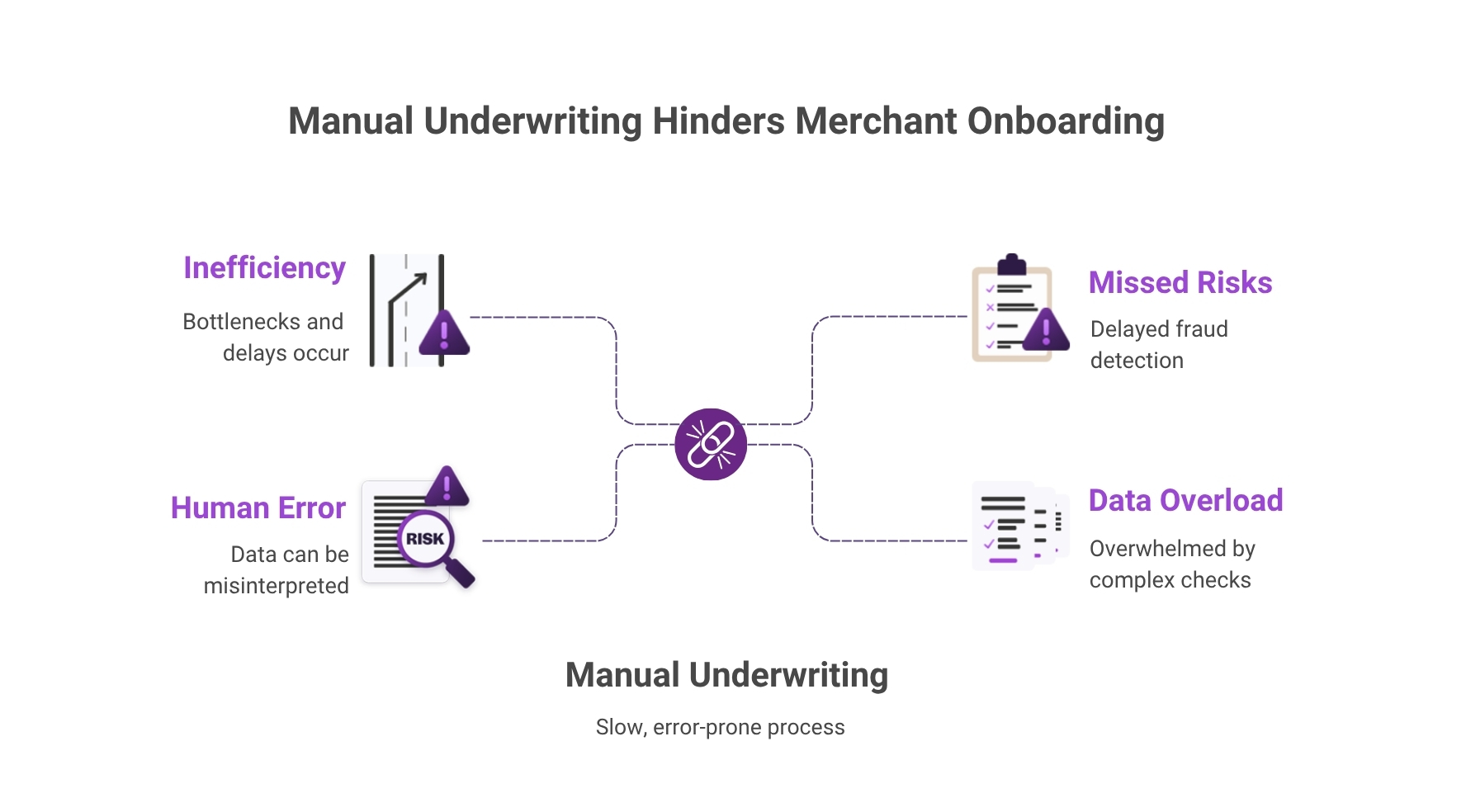

Challenges in Manual Merchant Underwriting

Manual merchant underwriting processes have long been part of risk management, but they create inefficiencies that slow teams down and weaken accuracy. For compliance officers, this means constant pressure, higher exposure to mistakes, and frustration when bottlenecks make it impossible to keep pace with growing demands.

Time-Consuming and Inefficient

Traditional underwriting often relies on paper-based systems or old technology, creating unnecessary delays. Merchants have to submit large amounts of documentation, which is then reviewed by hand. This slows down the onboarding process and impacts how quickly new accounts can be approved and revenue generated.

- Manual paperwork and reviews create bottlenecks.

- Lack of automation results in lengthy processes that can take days or weeks.

- The end result? Higher costs and slower service delivery.

Human Error and Inconsistent Decisions

The manual nature of underwriting exposes compliance and risk teams to constant risk of error, such as:

- Misinterpreting data can lead to poor decisions.

- Subjective judgments about financial stability create inconsistency.

- Inconsistent evaluations from different underwriters lead to varying outcomes.

Difficulty Spotting Red Flags in Real Time

Traditional underwriting leaves risk teams blind to emerging risks, such as:

- Delayed detection of fraud or suspicious activity.

- Red flags, like unusual transaction behaviour, may go unnoticed.

- This leaves providers exposed to higher risks as issues grow.

Complex Due Diligence and Data Verification

Merchant applications often require a thorough review of financial statements, tax filings, and ownership structures. Manually verifying all this information can overwhelm underwriters, leading to incomplete or inaccurate assessments.

- Cross-referencing multiple data sources complicates the process.

- Inaccurate assessments can arise from human oversight.

- Verifying ownership structures is time-consuming and prone to error.

These challenges make the underwriting process slow, resource-heavy, prone to mistakes, and hard to scale. As a result, payment providers and platforms struggle to keep up with the demands of a rapidly evolving digital landscape. Discover how our OnBoard simplifies the process.

Technology in Merchant Underwriting

The merchant underwriting process is undergoing a major shift with automation, AI, and digital merchant onboarding. For risk and compliance teams, this brings relief from overwhelming manual workloads and reassurance that fraud risks are spotted faster. It replaces uncertainty with consistency and confidence in every decision.

1. The Evolution of Technology in Underwriting

AI and machine learning have revolutionised merchant underwriting. The move from paper-based processes to automated systems has streamlined everything from data collection to risk assessment, ensuring decisions are quicker and more consistent.

Key Benefits:

- Speed and Efficiency: Automation handles large volumes of data swiftly, cutting processing times and allowing for faster onboarding decisions.

- Cost Reduction: By automating tasks that once required manual effort, businesses save on operational costs and can handle more applications without increasing headcount.

2. Automated Data Collection and AI-Powered Risk Evaluation

Automation and AI are reshaping how data is collected and analysed. With AI able to process large datasets in real-time, the risk evaluation process is faster and more accurate, and fraud detection becomes sharper over time.

Key Benefits:

- Accuracy and Consistency: AI reduces human error and bias by ensuring decisions are based on consistent, rule-driven systems.

- Improved Fraud Detection: AI’s ability to learn from new data means it continually enhances its fraud detection, identifying suspicious patterns or fraudulent documents before they escalate.

- Effective Risk Assessment: AI evaluates factors like a merchant’s financial health and chargeback history, creating accurate risk scores and helping to flag high-risk merchants early.

3. Integration with External Systems

Modern underwriting platforms now connect with third-party data sources, such as credit agencies and fraud detection services, making risk evaluation even more thorough.

Key Benefits:

- Advanced Fraud Prevention: AI systems can adapt to new fraud trends, predicting and flagging suspicious activities before they cause harm.

- Scalability: Automated systems can process vast amounts of data in real time, allowing businesses to scale without sacrificing accuracy or security.

By combining automation, AI, and machine learning, payment providers can enhance their risk assessment processes, speed up decision-making, and improve fraud detection—ultimately making the merchant onboarding process faster, more accurate, and cost-effective.

Improved Efficiency through Digital Onboarding

Digital merchant onboarding is transforming the merchant onboarding process. For compliance teams, what was once exhausting, error-prone work is now faster and more reliable. Automated checks reduce the stress of missed details, while streamlined workflows ease the burden of repetitive tasks and restore confidence in compliance outcomes.

Key benefits include:

- Simplified Data Collection: Digital onboarding removes the need for manual data entry by automatically collecting and verifying merchant details. This cuts down on administrative workload and accelerates processing times.

- Faster Approvals: Automation allows for real-time evaluation of merchant applications, enabling quicker decisions and reducing time-to-market for new merchants. This is particularly important in industries where speed provides a competitive edge.

- Less Paperwork: Traditional merchant onboarding often requires piles of paperwork and document handling. With the digital onboarding process, the paperwork load is greatly reduced, making the process more efficient and secure.

How Does Digital Onboarding Cut Down on Manual Tasks?

The digital onboarding process is designed to minimise the manual work involved in the merchant underwriting process, enabling payment providers to onboard merchants quickly while maintaining security and compliance.

- Automated Document Verification: Advanced systems automatically verify documents like business registrations, financial statements, and ID proofs. This reduces human error and speeds up the approval process.

- Instant Risk Assessment: Digital platforms assess merchant risk factors such as creditworthiness and fraud potential in real time, enabling payment providers to make informed decisions faster, without compromising security.

- Seamless Integration: With powerful APIs and integrations, digital onboarding platforms ensure smooth data transfers from external sources, cutting down on redundancies and administrative work. This improves overall operational efficiency.

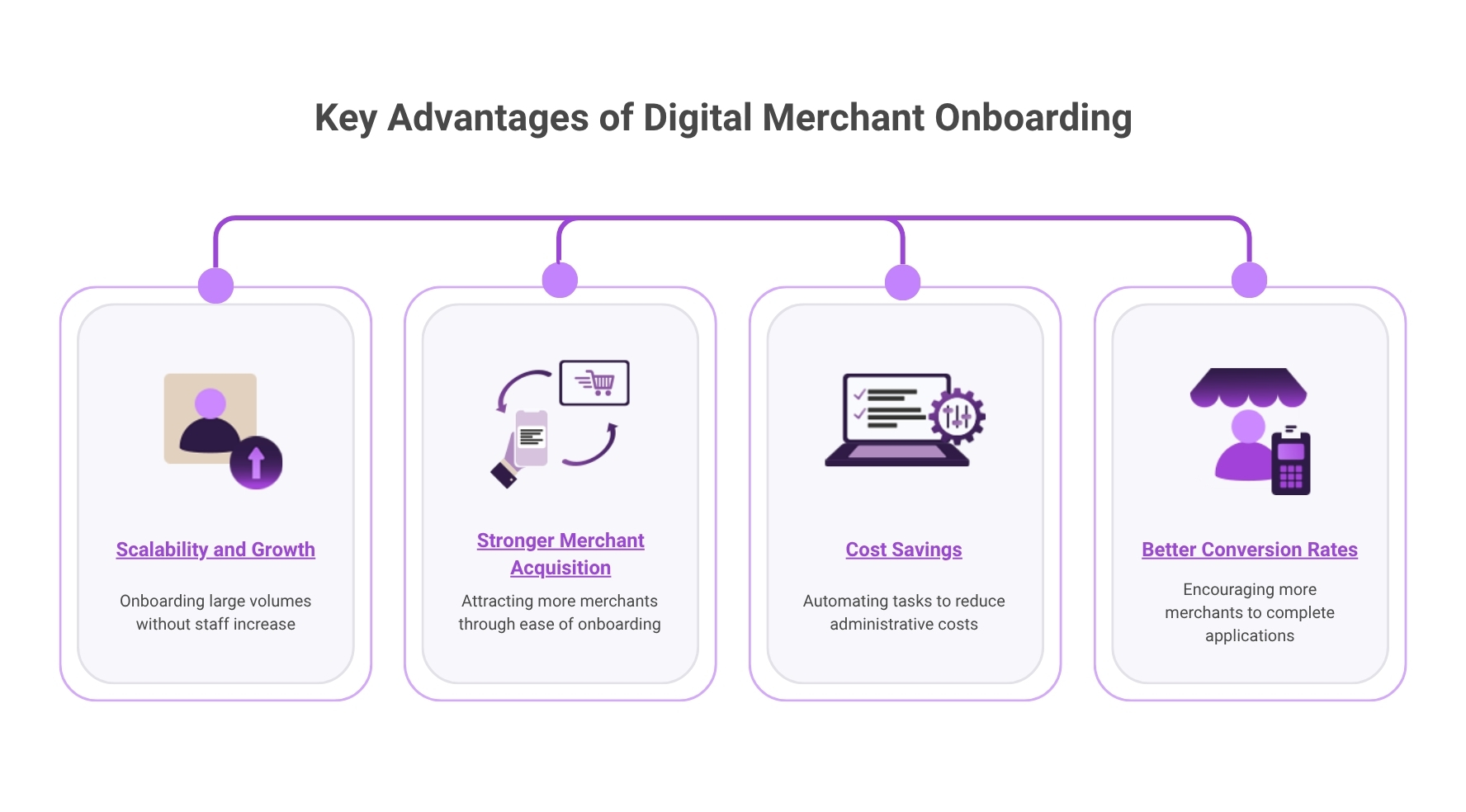

How Does Digital Onboarding Process Simplify Merchant Underwriting?

Adopting the digital onboarding process unlocks numerous opportunities for payment providers, helping them scale quickly while improving the experience for merchants.

- Scalability and Growth: Digital onboarding enables payment providers to onboard large volumes of merchants without needing to increase staff, supporting faster portfolio growth. This allows providers to expand into new markets with minimal additional cost.

- Better Conversion Rates: A smooth, user-friendly digital onboarding process encourages more merchants to complete their applications, leading to higher approval rates and a larger, more engaged customer base.

- Stronger Merchant Acquisition: Offering a fast, easy onboarding process attracts more merchants, enabling rapid expansion of the network. The digital onboarding process also allows for global merchant onboarding, removing geographical barriers and facilitating international growth.

- Cost Savings and Operational Efficiency: By automating repetitive tasks such as document verification, data entry, and background checks, payment providers can reduce administrative costs and boost profitability. These savings can then be reinvested into expanding services or improving customer experience.

In a world where digital solutions are becoming the norm, traditional merchant onboarding processes are quickly being replaced by the digital onboarding process. Payment providers who embrace the digital solutions not only streamline their operations but also position themselves to capture a larger share of the market, seize growth opportunities, and deliver a superior experience to their merchants.

Security and Risk Management

The integration of new technologies into the merchant underwriting process ensures that onboarding is not only secure but also fully compliant, safeguarding both merchants and providers. Some key features include:

- Biometric Verification: Sophisticated methods like facial recognition and fingerprint scanning add an extra layer of security during identity verification, making it much harder for fraudsters to pose as legitimate merchants.

- Real-Time Document Validation: AI-powered systems authenticate merchant-submitted documents in real-time, preventing fraudulent submissions from slipping through.

- Continuous Monitoring: Ongoing transaction and behaviour monitoring across digital platforms helps spot suspicious activity as it happens, enabling quick responses to potential security threats.

Balancing Speed with Risk Management with Digital Onboarding

While efficiency is crucial in digital payments, providers need to ensure that rapid onboarding doesn’t come at the expense of security or compliance. Digital onboarding platforms strike the right balance through the use of advanced AI and automation:

- Real-Time Risk Assessment: Automated systems instantly analyse merchant data to assess risk and flag high-risk accounts for further review, ensuring swift yet secure decisions.

- Automated Risk Scoring: AI generates detailed risk scores for merchants, helping providers prioritise higher-risk cases for closer inspection while keeping the overall process efficient.

- Customized Risk Profiles: Automated systems create risk profiles based on factors like a merchant’s industry, transaction history, and geographic location, improving fraud detection accuracy and reducing unnecessary delays.

By combining speed, accuracy, and ongoing monitoring, digital onboarding platforms enable payment providers to onboard legitimate merchants swiftly while keeping fraud risk in check—ensuring compliance and security throughout the entire merchant lifecycle. See how top providers balance speed with risk management in our guide Instant Onboarding at Scale: A Guide for Payment Providers.

Regulatory Considerations in Digital Onboarding

Compliance and regulatory considerations are one of the biggest priorities for risk and compliance teams. Digital onboarding ensures these requirements are met consistently and efficiently by:

- Automating KYC and AML Checks: Digital onboarding platforms automate the verification of merchants against national and international databases, ensuring all required KYC and AML checks are completed efficiently. This minimises human error and guarantees a consistent, accurate process.

- Real-Time Monitoring and Updates: Compliance is an ongoing responsibility. Digital platforms provide continuous monitoring of merchant activity, keeping businesses compliant throughout their relationship. Real-time updates ensure your business stays aligned with any regulatory changes.

- Audit Trails and Transparent Records: Digital onboarding generates clear, auditable records that offer complete transparency into the decision-making process. These records not only help meet regulatory requirements but also prepare your business for future audits, reducing the chance of penalties or violations.

Conclusion

The shift from traditional merchant underwriting to digital-first onboarding marks a significant change in how payment processing works. By leveraging AI, automation, and real-time data analysis, payment providers can make the onboarding process faster, more accurate, and better at managing risk.

Digital solutions help minimise human error, reduce fraud, and stay compliant with ever-changing regulations. As businesses look for scalable, secure solutions in a competitive market, digital-first onboarding offers a clear path for efficient growth, stronger merchant relationships, and a resilient approach to underwriting.

Adopting these technologies sets businesses up for long-term success, helping them stay ahead of the curve while keeping risk to a minimum.

Frequently Asked Questions

What Is the Merchant Underwriting Policy?

Merchant Underwriting Policy is the process financial institutions and payment processors use to evaluate a business before allowing them to accept payments. This policy ensures the merchants are legitimate, low risk, and compliant with KYC/AML regulations.

What is the Traditional Underwriting Process?

Traditional underwriting process often relies on paper-based systems or older technologies. Merchants usually have to submit large amounts of documentation, which is then reviewed by hand. This slows down the onboarding process and impacts how quickly new accounts can be approved and revenue generated.